Irs Section 368

Section 368 Tax Free Reorganizations For Federal Income Tax

Mere Change The New Final Section 368 A 1 F Regulations Ppt Video Online Download

Tax And Corporate Law On Sales And Purchases Of Businesses

Sample Merger Agreement Templates Di 2020

M A Tax For 2019

Stock For Stock Exchanges B And Triangular B Reorganizations

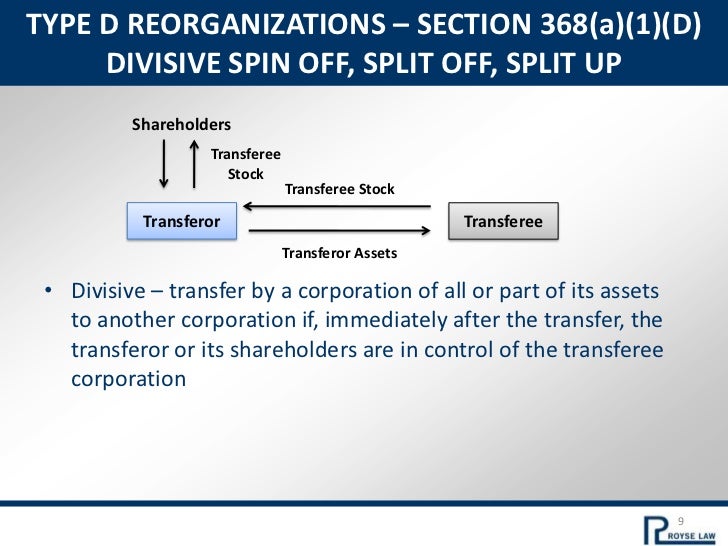

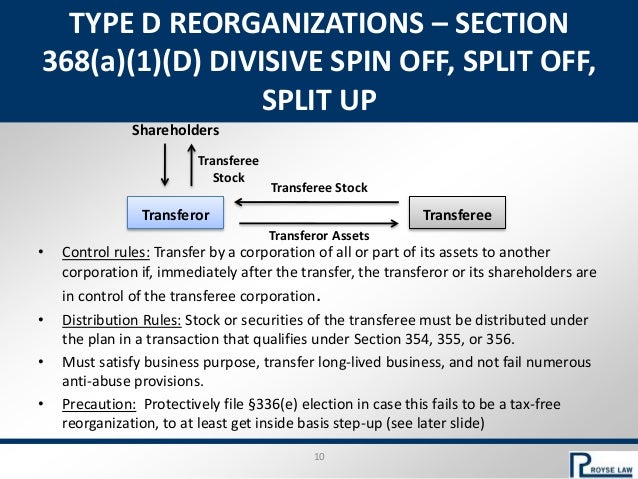

Section 368 outlines a format for tax treatment to reorganizations as described in the internal revenue code irc of 1986.

Irs section 368. Section 1 c of pub. Read the code on findlaw. These reorganization transactions however have to meet certain legal requirements to classify for favorable treatment.

22 1986 100 stat. 1954 as added by section 2131 a of the tax reform act of 1976 pub. Section 368 definitions relating to corporate reorganizations.

1954 as added by section 2131 a of the tax reform act of 1976 pub. Except that sections 367 d and 1492 of the internal revenue code of 1986. These reorganization transactions however have to meet certain legal requirements to classify for favorable treatment.

94 455 title xx 2131 a oct. 91 681 as amended by pub. Under 1 368 2 f of the income tax regulations if a transaction otherwise qualifies as a reorganization a corporation remains a party to a reorganization even though the stock or assets acquired in the reorganization are transferred in a transaction described in 1 368 2 k.

This document contains final regulations that provide guidance regarding the qualification of a transaction as a corporate reorganization under section 368 a 1 f by virtue of being a mere change of identity form or place of organization of one. Internal revenue code 26 usca section 368. 4 1976 90 stat.

4 1976 90 stat. Is a transaction in which 1 a parent corporation transfers all of the interests in its limited liability company that is taxable as a corporation to its subsidiary first. Managing a tax free reorganization is entirely dependent on the tax jurisdiction section 368 section 368 outlines a format for tax treatment to reorganizations as described in the internal revenue code irc of 1986.

Reverse Triangular Mergers A 2 E Reorganizations

International Tax Blog 368 Corporate Reorgs

Unsoved Crime Cold Case Www Facebook Com Send Tips Ammp Tips Gmail Com Cold Case Topeka Miss Kansas

Stock For Asset Exchanges C And Triangular C Reorganizations

Parts Of Indian Constitution Indian Constitution Ias Study Material Education Information

Https Www Irs Gov Pub Irs Wd 1224006 Pdf

Carnegie Museum Of Natural History Carnegie Museum Natural History Cone Snail

Mere Change The New Final Section 368 A 1 F Regulations

International Tax Advisory New Regulations On F Reorganizations News Insights Alston Bird

Https S2 Q4cdn Com 175866200 Files Doc Downloads Form8937 Tax1 Pdf

Https Marriott Gcs Web Com Static Files Cade2aee 40c9 42e6 803b 264135bd3cc3

Irs Form 926 Download Fillable Pdf Or Fill Online Return By A U S Transferor Of Property To A Foreign Corporation Templateroller

Https Www Irs Gov Pub Irs Drop N 09 78 Pdf