Section 152 Of The Internal Revenue Code

Domestic Partner Tax Dependent Declaration

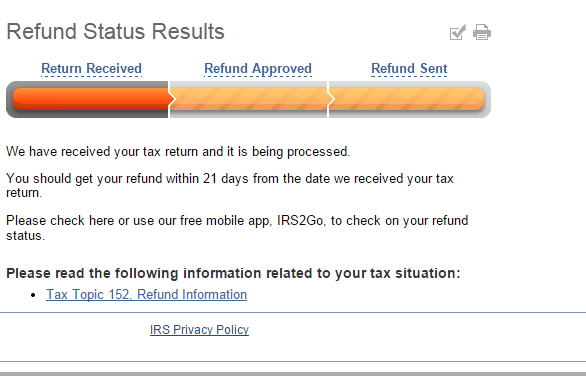

Irs Reference Codes On Where S My Refund Refundtalk Com

Family Education Rights And Privacy Act Ferpa Financial Information Release

A Research Example Tax Research Federal Guides At Georgetown Law Library

On The Irs Check My Refund Website It Says Tax Topic 152 Now After I Went Through A Very Gruesome Audit That Lasted Over A Year It Used To Say Tax Topic

3 12 37 Imf General Instructions Internal Revenue Service

/GettyImages-57173091-66f9b5d085fc4aa780d30dc7d2261489.jpg)

Section 152 d 1 d provides that an individual is not a qualifying relative of the taxpayer if the individual is a qualifying child of any other taxpayer.

Section 152 of the internal revenue code. Internal revenue code 26 usca section 152. Read the code on findlaw. B exceptions for purposes of this section 1 dependents ineligible if an individual is a dependent of a taxpayer for any taxable year of such taxpayer beginning in a calendar year such individual shall be treated as having no dependents for any taxable year of such individual beginning in such calendar year.

A in general for purposes of this subtitle the term dependent means 1 a qualifying child or 2 a qualifying relative.

Tax Implications And Rewards Of Grandparents Taking Care Of Grandchildren The Cpa Journal

Who Does The Irs Consider To Be A Qualifying Relative Accountingweb

3 12 179 Individual Master File Imf Unpostable Resolution Internal Revenue Service

Https Hr Umich Edu Sites Default Files Declaration Tax Status Oqa Pdf

Http Www Bradfordtaxinstitute Com Endnotes Irc Section 170b1a Pdf

Https Cao 94612 S3 Amazonaws Com Documents Deferred Comp Withdrawal Form Covid Related V2 Pdf

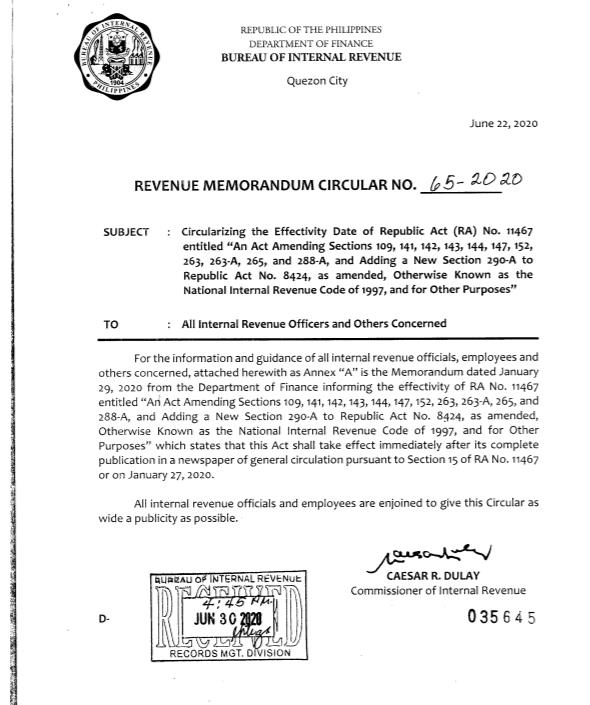

Ra No 11467 S Effectivity Date Is January 27 2020 Grant Thornton

Internal Revenue Code Irc

Internal Revenue Bulletin 2019 41 Internal Revenue Service

Refund Status Refundtalk Com

Irs Section 125core Documents

Https Www Lanl Gov Careers Employees Retirees New Hires Assets Docs 3027 Pdf

Https Tax Thomsonreuters Com Content Dam Ewp M Documents Tax En Pdf Brochures Checkpoint Catalyst Topics Brochure Pdf

Https Crsreports Congress Gov Product Pdf In In11358

Source : pinterest.com